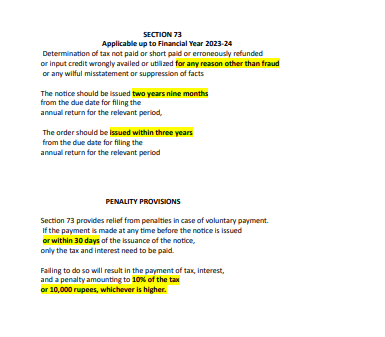

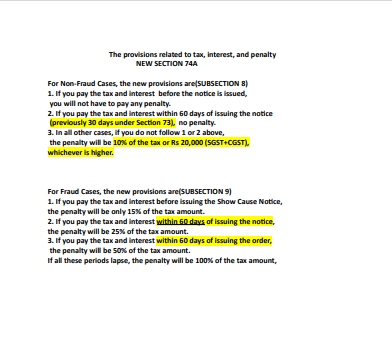

After section 128 of the Central Goods and Services Tax Act, the following section shall be inserted, namely:––

Waiver of interest or penalty or both relating to demands raised under section 73, for certain tax periods. “128A.

- Notwithstanding anything to the contrary contained in this Act, where any amount of tax is payable by a person chargeable with tax in accordance with,––

(a) a notice issued under sub-section (1) of section 73 or a statement issued under sub-section (3) of section 73, and where no order under sub-section (9) of section 73 has been issued; or

(b) an order passed under sub-section (9) of section 73, and where no order under sub-section (11) of section 107 or sub-section (1) of section 108 has been passed; or

(c) an order passed under sub-section (11) of section 107 or sub-section (1) of section 108, and where no order under sub-section (1) of section 113 has been passed,

Pertaining to the period from 1st July, 2017 to 31st March, 2020, or a part thereof, and the said person pays the full amount of tax payable as per the notice or statement or the order referred to in clause (a), clause (b) or clause (c), as the case may be, on or before the date, as may be notified by the Government on the recommendations of the Council, no interest under section 50 and penalty under this Act, shall be payable and all the proceedings in respect of the said notice 99 or order or statement, as the case may be, shall be deemed to be concluded, subject to such conditions as may be prescribed:

Provided that where a notice has been issued under subsection (1) of section 74, and an order is passed or required to be passed by the proper officer in pursuance of the direction of the Appellate Authority or Appellate Tribunal or a court in accordance with the provisions of sub-section (2) of section 75, the said notice or order shall be considered to be a notice or order, as the case may be, referred to in clause (a) or clause (b) of this sub-section

Provided further that the conclusion of the proceedings under this sub-section, in cases where an application is filed under sub-section (3) of section 107 or under sub-section (3) of section 112 or an appeal is filed by an officer of central tax under sub-section (1) of section 117 or under sub-section (1) of section 118 or where any proceedings are initiated under sub-section (1) of section 108, against an order referred to in clause (b) or clause (c) or against the directions of the Appellate Authority or the Appellate Tribunal or the court referred to in the first proviso, shall be subject to the condition that the said person pays the additional amount of tax payable, if any, in accordance with the order of the Appellate Authority or the Appellate Tribunal or the court or the Revisional Authority, as the case may be, within three months from the date of the said order:

Provided also that where such interest and penalty has already been paid, no refund of the same shall be available.

(2) Nothing contained in sub-section (1) shall be applicable in respect of any amount payable by the person on account of erroneous refund.

(3) Nothing contained in sub-section (1) shall be applicable in respect of cases where an appeal or writ petition filed by the said person is pending before Appellate Authority or Appellate Tribunal or a court, as the case may be, and has not been withdrawn by the said person on or before the date notified under sub-section (1).

(4) Notwithstanding anything contained in this Act, where any amount specified under sub-section (1) has been paid and the proceedings are deemed to be concluded under the said sub-section, no appeal under sub-section (1) of section 107 or sub-section (1) of section 112 shall lie against an order referred to in clause (b) or clause (c) of sub-section (1), as the case may be.”.